Bad banks- How Viable is the Idea?

From Current Affairs Notes for UPSC » Editorials & In-depths » This topic

IAS EXPRESS Vs UPSC Prelims 2024: 85+ questions reflected

In the wake of economic contraction and the concerns of an upcoming spike in NPAs, the Indian Banks Association proposed setting up a bad bank with a capital of 10,000 crore INR. This idea has been coming up every time a financial crisis threatens the banking sector. This time, the RBI has agreed to look into the possibility of establishing a bad bank- inviting criticisms from some sectors but encouragement from others.

What is a bad bank?

- Bad bank is a bank set up to buy bad loans and stressed assets without liquidity from other financial institutions.

- It is basically an asset reconstruction company (ARC) or an asset management company (AMC) that buys up the bad loans from a bank or a financial institution that has high proportion of NPAs or non-performing assets.

- This purchase is usually at prices below the book value of the loan.

- This bad loan is then managed by the bad bank until it recovers the money over a time period.

- This process clears up the balance sheet of the selling bank. However, the bank is required to take a haircut in this process.

- Bad banks are not involved in taking deposits or in lending. Their sole purpose is to soak up the bad loans from other banks and resolve them. They have been described as a ‘neelkanth’ to absorb the ‘poisoned stressed assets’.

- These are generally set up in times of crises in an attempt to recuperate financial institutions’ reputation and their wallet.

- The first such bad bank, Grant Street National Bank, was created in 1988 to clean up the Mellon Bank in the USA.

- The idea of bad bank was also famously used during the 2008 financial crisis to shore up private institutions with a lot of problematic assets.

- Bad banks have been formed elsewhere also. Eg: National Asset Management Agency of the Republic of Ireland, etc.

How did the idea originate in India?

- This idea was mooted as a PPP (public private partnership) in the 2016-17 Economic Survey as a way to tackle the ‘twin balance sheet’ problem.

- It was put forth in 2018 too but it didn’t take shape.

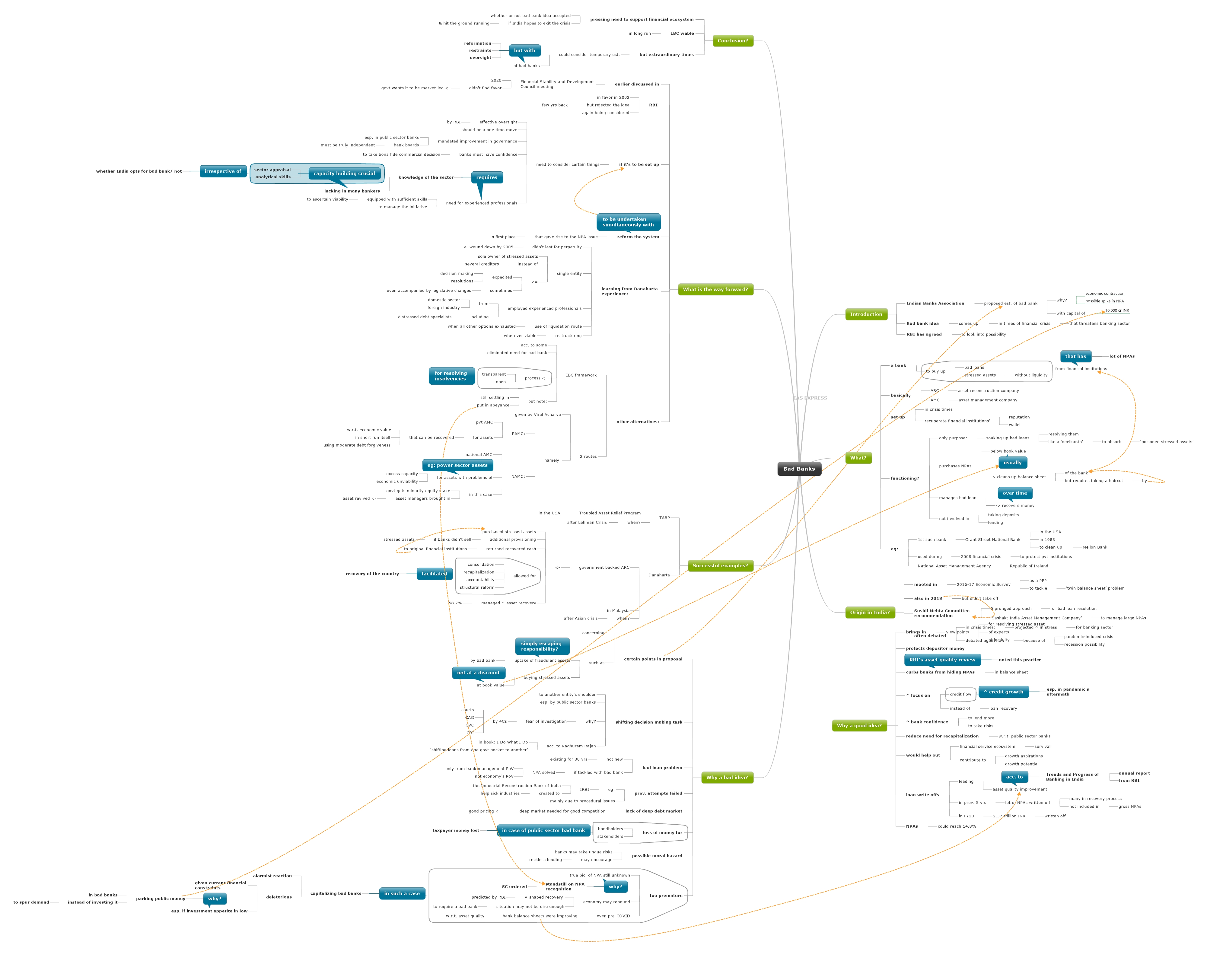

- The Sunil Mehta panel proposed a 5 pronged approach for bad loan resolution. It also proposed a ‘Sashakt India Asset Management Company’ to manage large NPAs.

- The idea often comes up for debate especially when the banking sector is looking at a projected rise in stress in the near term.

- The current pandemic-induced crisis has increased concerns about an impending recession, bringing with it the idea of bad bank into debate.

Why is it a good idea?

- The entity will help bring in an expert and objective view of the stressed asset problem.

- This could help prevent depositors from losing money.

- In previous asset quality review of banks conducted by the RBI, several banks were found to hide bad loans to show a healthy balance sheet. This practice can be discouraged if a bad bank is set up to clean up the balance sheets.

- It will enable banks to focus more on credit flow instead of focusing just on loan recovery. It will increase banks’ confidence to lend more and take risks.

- It could help boost credit growth– especially in the aftermath of the pandemic.

- It could also reduce the recapitalization requirement of public sector banks.

- The bad bank concept would not only help the financial service ecosystem survive but could also contribute to the growth aspirations and growth potential of India.

- Asset quality improvement has been led by write offs according to the Trends and Progress of Banking in India, an annual report from RBI. Over the last 5 years, a lot of NPAs have been written off. Many of these are still in the recovery process and don’t show up as gross NPAs. For example, the banks have written off 37 trillion INR in FY20.

- In addition to this, the NPAs could reach 8% according to RBI projections.

- Exploring bad bank idea could help the banking sector tide through such a scenario.

Why is it a bad idea?

- Concerns have been raised about certain points in the proposal for bad banks. Eg: uptake of fraudulent assets, buying of the stressed assets at book value instead of a discounted value, etc. This has led some to consider the idea as simply escaping responsibility.

- Some opine that the idea of bad bank is like ‘kicking the can somewhere else’ i.e. shifting the decision making task on stressed assets to some other entity’s shoulder. This tendency, especially among public sector banks, arises from the fear of investigations by the 4Cs:

- Raghuram Rajan, in his book I Do What I Do, criticised the idea as just ‘shifting loans from one government pocket to another’. He questioned how this strategy could improve matters.

- The bad loan problem in India is not a new one, we have been struggling with it for 3 decades And the use of bad bank solves the NPA issue only from the bank management point of view– not the economy’s point of view.

- Previous attempts, like the Industrial Reconstruction Bank of India (IRBI) that was created to help out sick industries, have failed in India. This failure was mainly due to procedural issues.

- The idea of bad bank would work best if India has a deep debt market with ARCs competing against each other to enable good pricing. Unfortunately, India doesn’t have this.

- Though the bad bank idea can protect the depositor money, the shareholders and bondholders stand to lose money. In case of the bad bank being in the public sector, the taxpayer money would be lost.

- Critics have argued that these banks could lead to a moral hazard as it may encourage financial institutions to take undue risks knowing that a bad bank bailout would serve as a safety net.

- In some countries, the idea has resulted in encouraging reckless lending.

- Some say that setting up a bad bank now would be too premature as the true picture of NPAs is yet to be seen- given that the Supreme Court-ordered standstill on NPA recognition is still in place.

- If the economy were to rebound in the first half of FY21, in a V shaped curve as suggested by the RBI, the situation may not be dire enough to require a bad bank.

- Even prior to the COVID-induced economic downturn, the bank balance sheets were beginning to improve with regards to asset quality.

- In such a case, capitalizing bad banks generously could be an alarmist reaction according to some critics.

- This would be especially deleterious given the current financial constraints.

- If the post-COVID investment appetite is low, parking public money in bad banks instead of investing it to spur demand would turn out to be a bad call.

Are there any successful examples?

- The TARP or Troubled Asset Relief Program that was introduced after the Lehman Crisis in the USA is considered a success story.

- The Malaysia set up the Danaharta, a government backed ARC in the aftermath of the Asian crisis. It purchased stressed assets from financial institutions and imposed additional provisioning if the banks don’t sell their assets.

- The recovered cash was returned to the original financial institutions. It allowed for broad consolidation, recapitalization and accountability. It also allowed structural reform of the financial institutions which then went on to facilitate the country’s recovery from the Asian crisis.

- The Danaharta experience is widely considered a successful example of a bad bank. It managed a 58.7% asset recovery– highest among the Asian countries.

What is the way forward?

- The idea was discussed at the Financial Stability and Development Council meeting in 2020, but didn’t find favour. The government stand has been that bad loan resolution should be market-led.

- The RBI was in favour of the ARCs in 2002 but rejected the bad bank idea a few years back. However, the idea is being considered by the central bank.

- If it were to be set up, certain things have to be considered going forward.

- RBI should have an effective oversight over the initiative.

- If India chooses to set up a bad bank, it should be a one-time move.

- Improvement of governance must be mandated. The bank boards– especially of the public sector banks- must be made truly independent to address the issue of governance. The banks must be given the confidence to take bona fide commercial decision.

- Several Indian experts have also highlighted the need to have experienced professionals, equipped with sufficient skills to ascertain a unit’s viability, manage this initiative. This requires knowledge of the unit’s sector and many bankers are deficient with regards to this.

- Irrespective of whether or not India opts for the bad bank route, developing better capacity for sector appraisal and analytical skills among the lenders is vital.

- Also the system that initially gave rise to the NPA problem originally must be reformed for pulling out the issue by its root. This structural reform must be simultaneously implemented along with the bad bank.

- Certain learnings from the Danaharta experience could be noted for emulation:

- It wound down in 2005 i.e. didn’t last for perpetuity.

- A single entity was the sole owner of a stressed asset instead of the asset being coordinated among several creditors. This helped in expediting decision making and resolutions. Sometimes, these were accompanied by legislative changes.

- The Danaharta employed experienced industry professionals– both from the domestic sector and from foreign industry. They also included distressed debt specialists.

- Liquidation route was used only when all other efforts failed and restructuring was used wherever viable.

- There are also other alternatives:

- Many argue that the IBC framework has removed the need for a bad bank. The IBC itself provides a process that is transparent and open- enough for resolving insolvencies. However, this system is still settling in and moreover, has been put in abeyance.

| Recovery method | Average recovery |

| Via IBC | 42.5% |

| Via SARFAESI | 14.5% |

| Via Lok Adalats | 5.3% |

| Via Debt Recovery Tribunals | 3.5% |

- Viral Acharya, former Deputy Governor of RBI, proposed 2 ways of resolving bad loans:

- A private asset management company (PAMC)– could be used if the stress is such that the assets could recover economic value in the short run itself with just a moderate level of debt forgiveness.

- A national asset management company (NAMC)- could be used if the issue is not just excess capacity but also economic unviability of the assets. Eg: Power sector. The NAMC raises debt to finance the asset and the government would have a minority equity stake in it. Then asset managers could be brought in to revive the asset.

Conclusion

Whether or not the RBI decides to establish a bad bank, there is a pressing need for supporting the financial ecosystem in India if it hopes to come out of the pandemic induced crisis to hit the ground running. The IBC is a viable route in the long run. But to address things in these extraordinary time, a temporary establishment of bad banks can be considered- but with appropriate attempts at reformation, restraints and oversights.

Practice question for mains

NPAs in India could rise as high as 14% as a result of the pandemic induced economic crisis. In this context, examine the need for setting up a bad bank. (250 words)

If you like this post, please share your feedback in the comments section below so that we will upload more posts like this.