Sovereign Green Bond- Pros, Challenges and the Way to Greenium

From Current Affairs Notes for UPSC » Editorials & In-depths » This topic

IAS EXPRESS Vs UPSC Prelims 2024: 85+ questions reflected

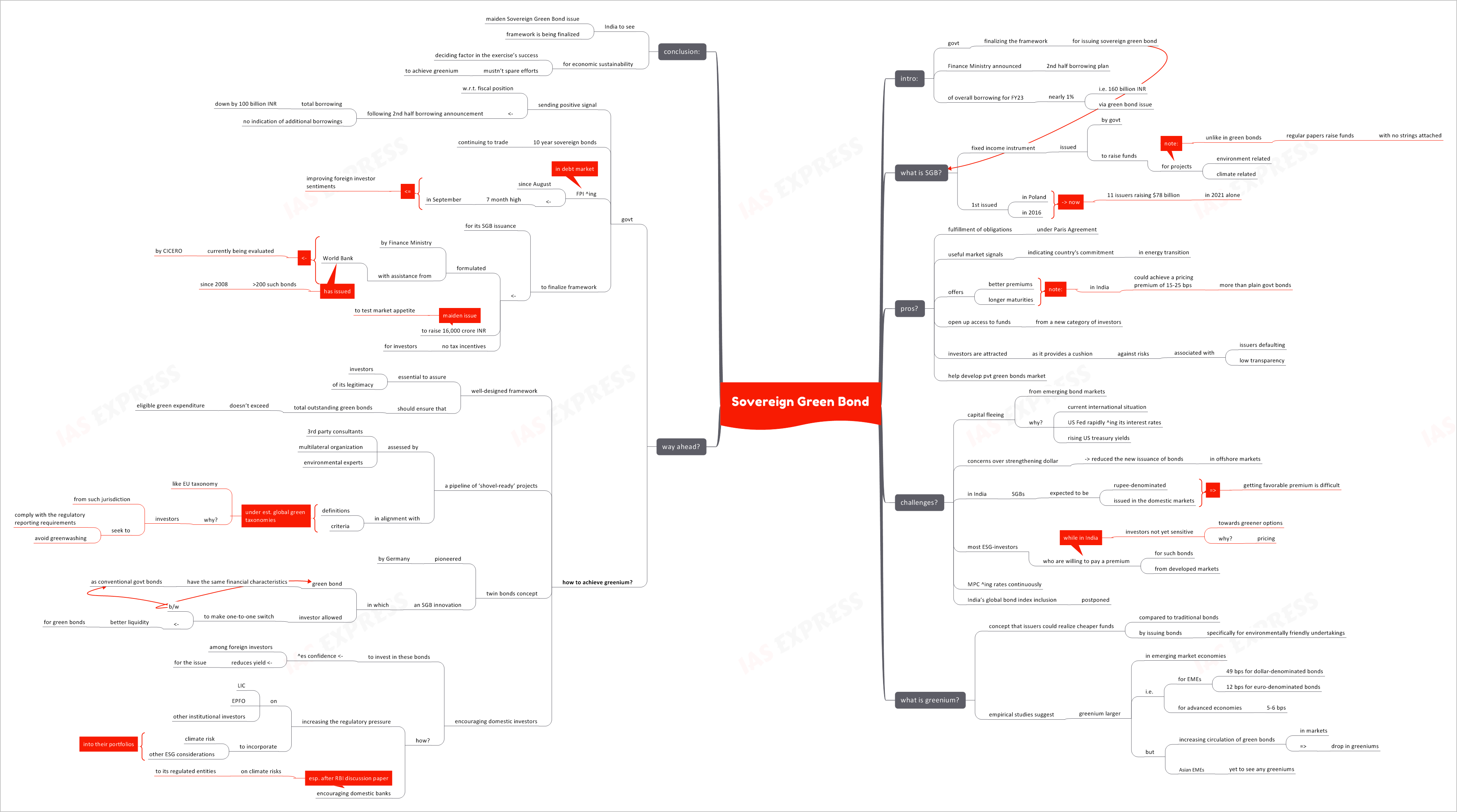

The government is finalizing the framework for issuing sovereign green bond. Recently, the Finance Ministry announced the 2nd half borrowing plan. Of the overall borrowing for FY23, nearly 1% i.e. 160 billion INR is to be via green bond issue.

What is SGB?

- Sovereign green bond is a fixed income instrument, issued by the government, to raise capital for environment- or climate-related projects.

- Unlike in case of green bonds, regular papers raise funds that have no strings attached i.e. can be used for any kind of project.

- SGBs were first issued by Poland in 2016. Since then the market has grown rapidly with 2021 alone seeing 11 issuers raising $78 billion cumulatively.

What are the pros?

- SGBs help countries finance undertakings towards the fulfilment of their obligations under the Paris Agreement framework.

- They serve as useful market signals, indicating that the issuing country is committed in its energy transition efforts.

- SGBs offer better premiums and longer maturities. For the Indian government, these bonds could achieve a pricing premium of 15-25 bps more than the plain government bonds.

- They open up access to funds from a new category of investors.

- Investors are attracted to this instrument as it provides a cushion against risks associated with issuers defaulting and low transparency.

- Issuing SGBs help develop the private green bonds market.

What are the challenges?

- Capital is fleeing from the emerging bond markets due to the current international situation, added to by the US Federal Bank rapidly hiking its interest rates and the rising US treasury yields.

- Concerns over the strengthening dollar has reduced the new issuance of bonds in offshore markets.

- Meanwhile, the SGBs that the Indian governments are set to issue are expected to be rupee-denominated and issued in the domestic markets. This means that achieving a favourable premium is likely to be a difficult task.

- Most of the ESG (environmental, social and governance)- oriented investors, who are willing to pay a premium for such sustainable bonds, are from the development markets. Indian investors, however, are yet to show sensitivity towards greener options, especially given the pricing.

- The Monetary Policy Committee has been increasing the rates continuously.

- There is also the issue of India’s global bond index inclusion being postponed adding to the challenges.

What is greenium?

- Greenium is a concept that issuers would be able to realize cheaper funding, compared to traditional bonds, by issuing bonds specifically for environmentally friendly undertakings.

- Empirical studies of greenium in SGB issuance suggests that it is larger for emerging market economies.

- The greenium estimates for such markets are 49 bps for dollar-denominated bonds and 12 bps for euro-denominated bonds.

- Comparatively, the advanced economies’ greenium estimates stand at 5-6 bps.

- However, there is a possibility that increasing circulation of green bonds in the market could have triggered the drop in greeniums.

- Also, Asian EMEs are yet to see any greeniums.

What is the way ahead?

- The government has been sending a positive market signals with regards to its fiscal position. Following the 2nd half borrowing announcement, the total borrowing has come down by 100 billion INR and there aren’t any indications of additional borrowings.

- Despite the adverse international economic situation, India’s 10 year sovereign bonds continue to trade.

- Since 2022, the FPIs in the country’s debt markets have increased and September numbers was a 7-month high. This is an indication of improving foreign investor sentiments.

- The government is expected to finalize the framework for its SGB issuance in the near future.

- It aims to raise 16,000 crore INR through this issuance in the 2nd half of FY23.

- It isn’t expected to provide tax incentives to attract investors into the segment.

- The framework, formulated by the Finance Ministry with assistance from the World Bank, is currently being evaluated by CICERO, a top global independent reviewer of green investment architecture. Note that the World Bank has issued over 200 such bonds since 2008.

- This maiden issuance is mainly to test the market appetite for these sustainable instruments.

How can India achieve greenium?

- A well-designed framework is essential to assure the investors of its legitimacy.

- In addition to this, readying a pipeline of ‘shovel-ready’ projects that follow the bond framework is necessary. These projects can be assessed by 3rd party consultants, multilateral organization and environmental experts.

- These projects must be in alignment with the definitions and criteria under established global green taxonomies, like the EU taxonomy. Investors from such jurisdictions seek to invest in projects that align with established taxonomies, in order to comply with the regulatory reporting requirements, while avoiding green-washed projects.

- The framework should ensure that the total outstanding green bonds doesn’t exceed the eligible green expenditure.

- The concept of twin bonds, pioneered by Germany, is SGB innovation worth considering. In this concept, the green bonds have the same financial characteristics as the government’s conventional issues. This system allows investors to make one-to-one switch between the green instrument and its conventional twin at any time, thus enabling liquidity for green bonds.

- When domestic investors exhibit higher demand for these bonds, foreign investors’ confidence would be boosted and would eventually help reduce the yields for the issue.

- The domestic demand for the SGBs can be boosted by increasing the regulatory pressure on LIC, EPFO and other institutional investors to incorporate climate risk and other ESG considerations into their portfolios.

- Domestic banks should be encouraged to diversify their portfolios too. This would encourage them to participate in the SGBs issue. The fact that RBI highlighted the climate risks threatening its regulated entities, in its discussion paper, should serve as a nudge in the right direction.

Conclusion:

India is set to see its maiden Sovereign Green Bond issue and towards this a framework is being finalized. While this will take India closer to achieving its objectives under the international climate action project, economic sustainability is also a deciding factor in the exercise’s success. Hence, the government mustn’t spare efforts to achieve greenium.

Practice Question for Mains:

Explain the concepts of ‘Sovereign Green Bonds’ and ‘greenium’. What can be done to achieve greenium in India? (250 words)

If you like this post, please share your feedback in the comments section below so that we will upload more posts like this.