National Health Protection Scheme (NHPS) – All you need to know

From Current Affairs Notes for UPSC » Editorials & In-depths » This topic

IAS EXPRESS Vs UPSC Prelims 2024: 85+ questions reflected

Updates *

What is the National Health Protection Mission (NHPM)?

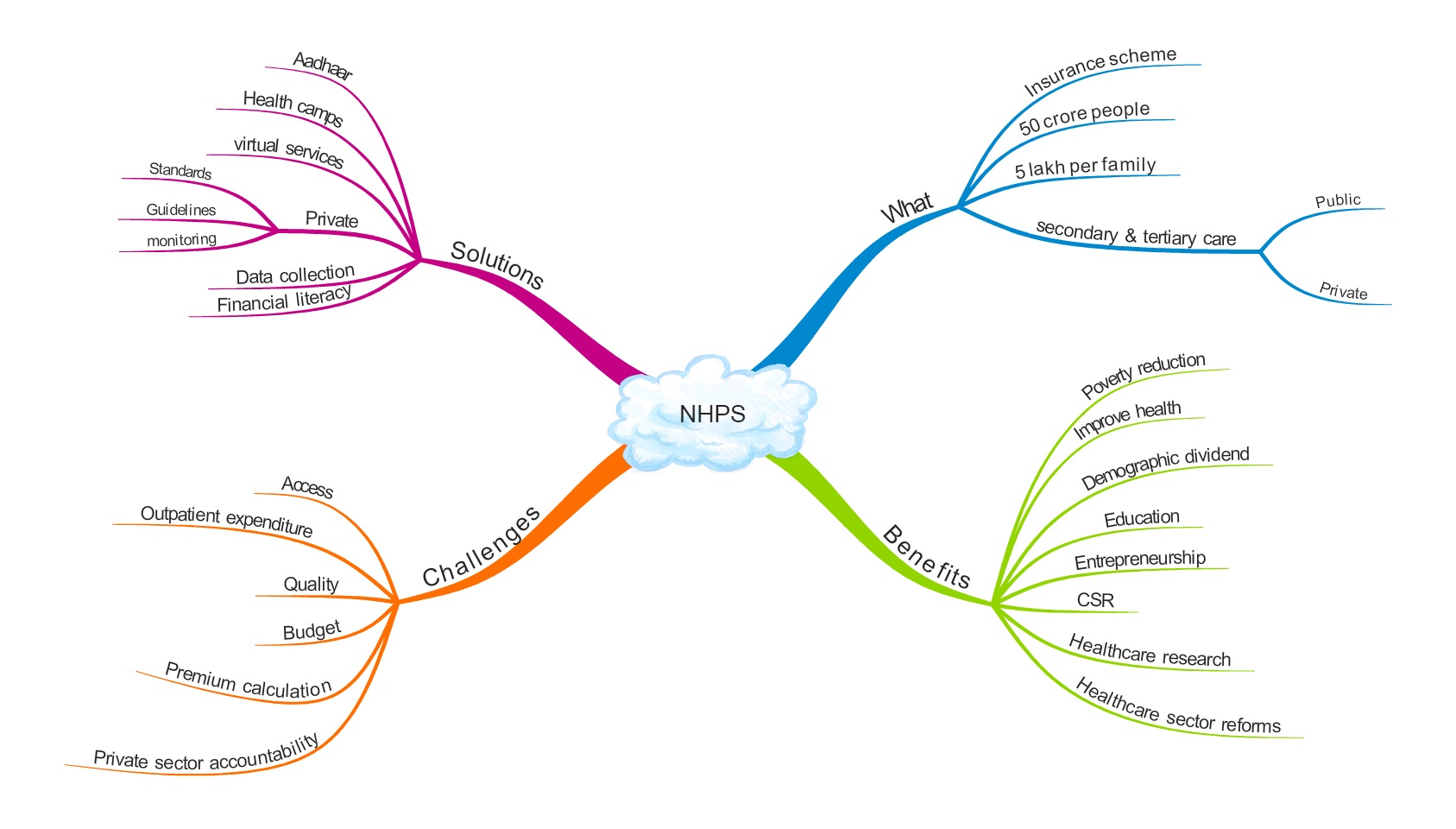

- NHPS is a health insurance scheme which seeks to provide insurance coverage to approximately 50 crore people (with focus on 10 crore poor and vulnerable families) of up to 5 lakh rupees per family per year against hospitalization expenses in secondary and tertiary care.

- It is a part of PM Jan Arogya Yojana (Ayushman Bharat Programme) which consists of NHPM and wellness centres programme. Ayushman Bharat is the world’s largest government-funded healthcare programme. *

- While NHPS serves secondary and tertiary health care needs, wellness centres will serve primary healthcare needs which is the first line of contact to people, particularly in rural India.

- It will subsume existing centrally sponsored insurance schemes such as Rashtriya Swasthya Bima Yojana (RSBY) and the Senior Citizen Health Insurance Scheme (SCHIS).

Why NHPS?

- According to the National Sample Survey Office report of 2014, India’s out of pocket expenditure for healthcare services are extremely high of about 70% which pulls approximately 7% of the population into poverty.

- According to SECC data (2011), 21% of annual income was lost due to diseases particularly among the poor and vulnerable population in rural and urban areas.

- The public health expenditure (total of centre and state governments) in India is only about 1.3% of GDP which is very low compared to other nations such as the USA which spends 18% of GDP.

- With increased insurance coverage to nearly 40% of the population particularly the poorest and the vulnerable in secondary and tertiary healthcare, the NHPS will result in the reduction of poverty and improved access to quality health and medication.

Where will it be implemented?

NHPS will be launched across all States/UTs and in all districts with an aim to cover all the targeted beneficiaries.

What are the entitlements under the scheme?

- NHPS will have a defined benefit cover of Rs. 5 lakh per family per year.

- Beneficiaries are entitled to cashless benefits from any public/private hospitals throughout the country.

- Cashless benefits include all investigations, medicine, pre-hospitalization expenses, etc. It would also cover pre-existing illnesses.*

Who are the targeted beneficiaries and how will they be identified?

- NHPS will target about 10 crores poor, deprived rural families and identified occupational categories of urban workers’ families.

- The identification will be based on the latest Socio-Economic Caste Census (SECC) data covering both rural and urban areas.

- The scheme is dynamic in identification by taking into consideration any changes in the future SECC data such as inclusions, exclusions, deprivations, and occupational criteria.

- No cap on the family size and age.*

How will it be implemented?

- One of the main principles of NHPS is cooperative federalism as it provides flexibility to states in the implementation of the scheme.

- At the national level, an Ayushman Bharat National Health Protection Mission Agency (AB-NHPMA) will be established to manage and coordinate the mission.

- At the state/UTs level, State Health Agency (SHA) would be established for the implementation. SHAs can be an existing trust, society, non-profit company, state nodal agency or a new entity set up for the purpose of the scheme.

- States/UTs have the option to choose whether they want to implement the scheme through an insurance company or through SHA or an integrated model.

- The expenditure incurred in the payment of premium by beneficiaries will be shared between Central and State governments in a pre-determined ratio – 60% will be borne by Centre and 40% by states. *

- Funds will be transferred from AB-NHPMA to SHAs directly through an escrow account.

How is NHPS different from Rashtriya Swasthya Bima Yojana (RSBY)?

Both NHPS and RSBY are health insurance schemes targeting poor and vulnerable sections. But there are certain differences as follows

- RSBY was based on enrolment, but NHPS is based on entitlement. This means that in NHPS, the identified population has to be merely informed about their entitlement to health insurance benefits under the scheme, instead of paying the premium to insurers, spreading awareness and sensitisation of target population like that of RSBY. This will lead to automatic coverage of all the identified sub-groups in the populations under NHPS once the scheme is operational.

- It doesn’t have limitations of RSBY. For instance, RSBY provides the cover of only Rs. 30,000 for a family of five and it did not include outpatient care.

- A study reveals that an increase in outpatient expenditure, hospitalisation and medicines forced insurance companies under RSBY to remove several diseases out of their policies and thus making it unaffordable for BPL families. Since NHPS is fully subsidised by the Central and State government through their budgetary support rather than through insurance companies, such instances might not occur in NHPS implementation.

What are the benefits of NHPS?

- Reduces poverty: NHPS will resolve the problem of out of pocket expenditure, thus reducing poverty and improving the health of poor and vulnerable households. Hence, NHPS is an important move towards universal health coverage.

- Improves health: It will lead to timely treatments, improved health outcomes, patient satisfaction due to better access to secondary and tertiary hospitals.

- Demographic dividend: Since diseases cured are work days gained, NHPS will improve the productivity of workers and reduce wage losses.

- Employment: As the scheme improves the affordability of healthcare, around 50 crore population will have demand for insurance. This will serve as an opportunity for insurance companies to expand even in tier 2 and 3 cities and will create additional employment and revenue.

- Education & Entrepreneurship: With the reduction in out of pocket expenditure for healthcare needs, beneficiaries can invest their hard earned money in the education of their children or in entrepreneurship activities which will further create employment opportunities in India.

- Corporate Social Responsibility (CSR): Government expects contribution from the private sector through CSR and philanthropic institutions. Hence it serves as an opportunity for companies which are mandated to spend at least 2% of the average net profit on CSR activities under the companies act, 2013.

- Reforms in the healthcare sector: NHPS will induce long-pending reforms in the healthcare industry such as standardisation of treatment protocols and care, categorisation, rationalisation of cost and creation of separate healthcare inflation index. It can be used to increase transparency by providing data on quality of care from different hospitals or clinics in India.

- Healthcare research: NHPS will have access to health data of 50 crore people. This data can be used effectively for research or understanding which treatments work better in the real world rather than just through clinical trials. It can be used to generate personalized and precision medicine for treatment based on individual genetic or other characteristics.

What are the disadvantages/challenges in the implementation of NHPS?

- The Rs 5 lakh cover is intended only for secondary and tertiary care hospitalisation.

- NHPS is seen as a visionary, populist, ineffective solution for universal healthcare, a pro-private, scaled-up version of old schemes, pre-election move, etc.

- Rural people find it difficult to travel to hospitals (public or private) which lies miles away. So, it is not a matter of choice, but the difficulty in getting access to secondary and tertiary care.

- The pursuit of health may trap the poor and deprived households in medium or long-term treatments, which would exponentially increase their out of pocket expenditure further. Hence they won’t seek healthcare due to this threat.

- There are still people who don’t trust the quality of health care due to rising medical failures and hence they believe that it doesn’t worth their expenditure.

- NHPS doesn’t cover outpatient services in the private healthcare sector. However, the top diseases that add maximum burden on out of pocket expenditure are from diseases including bronchitis and asthma, tuberculosis, diarrhoea, etc. which requires regular outpatient consultations and are largely provided by private sector only.

- NHPS will require the government to increase its current spending of 1.4% of GDP to at least 10% to cover all the intended beneficiaries and to provide quality infrastructure for the services under the scheme. It is not clear how the government would raise such money.

- There is a challenge in integrating the insured, insurers, the state, and the healthcare providers.

- The premiums to fund the NHPS are still not decided and there are varied perspectives on premiums calculation among politicians, insurers and doctors.

- Private healthcare has been known to exploit people and will also try to exploit NHPS. NHPS doesn’t provide any guidelines to regulate the private in NHPS implementation.

- Moreover, the private sector’s willing participation is unlikely since the prices proposed under the rate card is much below the expectations of private sector healthcare providers.

- Preparing the entire medical procedure list at the central level is an ineffective move due to the varied healthcare needs and disease prevalence across the nation.

What should be the government’s move?

- There is a need to streamline the enrolment process by reducing the number of forms or incorporation of Aadhaar for enrolment purposes. For this, Aadhaar should cover all the population who are yet to be covered.

- After the enrollment, access to health care should be provided to people where they live. For this purpose, super specialty hospitals in cities can organise health camps in rural areas and also initiate virtual healthcare services at primary health centres in rural areas.

- In addition to targeting the poor and vulnerable populations, the scheme should also target various health conditions where disease burden is high.

- To ensure the accountability of private hospitals in the implementation of NHPS, the government should come up with detailed guidelines, quality standards, and monitoring mechanism. Also, there should be a prior authorization procedure for expensive medical surgeries.

- Health data on the region, age, season-wise disease trends, inpatient and outpatient attendance at primary to tertiary care must be collected and stored digitally. It is because accurate data on health care will provide insurance companies to arrive at a balanced formula for premiums calculations for basic treatment to complex surgeries.

- Preventive care should also be given due focus to reduce the disease burden in the country.

- The utilisation of NHPS should be improved with effective education and financial literacy campaign. Social media can be effectively used for this purpose.

- Disease & state specific interventions needed. And the states’ role has to be enhanced at the planning stage itself and could be given the responsibility to prepare the medical package list. Further, if the poorer states could fix high prices for healthcare packages, it could increase private investment in those states.

Conclusion

“Health Insurance is a right, not a privilege”. Hence NHPS is a step in the right direction to provide universal healthcare. NHPS is not just a health insurance scheme that offers financial protection but also has the potential to induce the much-needed reforms to strengthen India’s health sector. If implemented effectively, it will be a game changer for India’s healthcare sector and the economy as a whole.

Updates *

On 2 January 2019 Centre government approved the restructuring of the existing National Health Agency as the ‘National Health Authority’ for better implementation of PM-JAY. Therefore with this approval, the existing society “National Health Agency” was dissolved and was replaced by the National Health Authority.

The National Health Authority is an attached office to Union Ministry of Health & Family Welfare.

NHA has full accountability, authority and mandate to implement PM-JAY through an efficient, effective and transparent decision-making process.

Overview

If you like this post, please share your feedback in the comments section below so that we will upload more posts like this.

What you said is correct ….It has to be EFFECTIVELY IMPLEMENTED …

ayusman card