RBI on Green Deposits- Highlights, Significance & Challenges

From Current Affairs Notes for UPSC » Editorials & In-depths » This topic

IAS EXPRESS Vs UPSC Prelims 2024: 85+ questions reflected

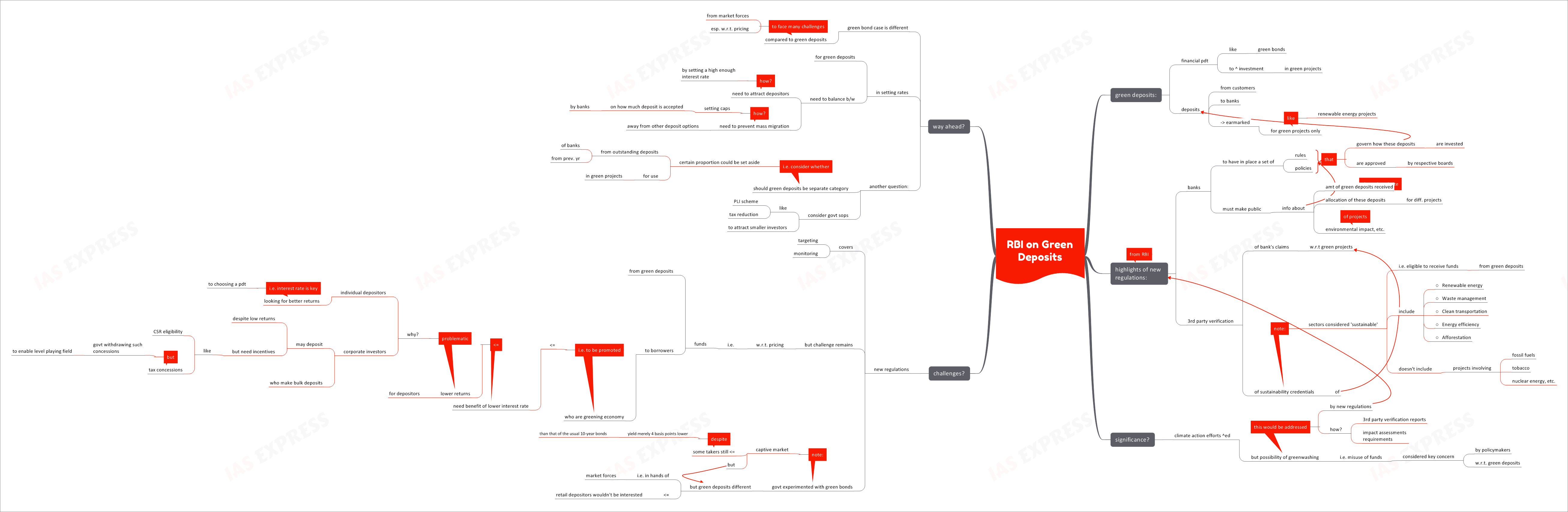

The Reserve Bank of India has come up with a regulatory framework for green deposits. While the government has previously experimented with the sovereign green bonds, the new regulation faces a very different set of challenges as the market forces will a significant say in the green deposits’ success.

What are green deposits?

- Green bond is one of the many financial products (like green bonds) that are used to invest money in environmentally sustainable projects.

- These are deposits accepted by banks from customers and earmarked for environmentally-friendly projects.

- For instance, a bank may accept green deposit from customers and use it to invest in renewable energy projects.

What are the new regulations?

The RBI has issued a regulatory framework to govern the green deposit facility offered by banks.

- The banks are to put in place a set of rules and policies to govern how they invest the green deposits. These need to be approved by their respective Boards.

- These rules must be made public through their respective websites.

- The banks are to regularly disclose information like:

- Amount of green deposits received

- Allocation of these deposits for green projects

- Environmental impact of such investments, etc.

- A 3rd party must verify:

- The banks’ claims regarding the green projects they invest in

- Sustainability credentials of these projects

- The RBI has listed the sectors that would be considered ‘sustainable’ and hence, eligible to avail investments of green deposits. These include:

- Renewable energy

- Waste management

- Clean transportation

- Energy efficiency

- Afforestation

- The banks mustn’t invest the green deposits in projects involving:

- Fossil fuels

- Nuclear power

- Tobacco, etc.

Why is it significant?

- Investing in green projects is one of the best ways when it comes to climate action. However, there are concerns that banks and other financial entities could misrepresent the actual environmental benefit of the projects they route these funds to.

- Policymakers consider the use of funds to be the main issue in this equation. The new regulations seek to prevent green-washing i.e. misleading customers into believing that certain business projects are environmentally sustainable.

- This would be ensured by the measures like 3rd party verification reports and impact assessments requirements.

What are the challenges?

- While the new regulations cover targeting and monitoring the use of green deposits, the challenge that remains is raising these deposits in the first place.

- This is because of the issue of pricing. The borrowers of these funds are helping green the economy and would hence, have the benefit of lower interest rates. However, this would mean that the depositors would get a lower interest on green deposits, compared to that on regular deposits.

- At a time when individual deposit holders are struggling to get better returns on their interest, the interest rates offered by the banks would be a key deciding factor when choosing banks and financial products. In this context, the green deposits would not make much sense to the individual.

- Even in the case of bulk deposits from corporates, green deposits with low returns would make sense only if there are sufficient regulatory set-offs- like fulfilment of requirements under CSR (corporate social responsibility) or tax concession. However, the government is currently withdrawing such tax benefits in pursuit of ‘level playing field’ for all savings and investments.

- If the government’s experiments with green bonds are any indication of the demand for green instruments in the market, there is a risk of low response in the case of green deposits too. Note that even the institutional investors didn’t find the green bonds, with a yield merely 4 basis points lower than that of the usual 10-year bonds, there is less reason to expect retail investors to opt for green deposits.

What is the way ahead?

- It must be remembered that the sovereign green bond still has takers as it is a captive market situation. This is not the case for green deposits. Here, the market forces will have a decisive role and will relentlessly test the pricing mechanism.

- Solving the pricing issue is key to the success of green deposits. Care must be taken to balance the need to attract depositors (by setting a high enough interest rate) and the need to prevent mass migration away from other deposit options (by setting caps on how much deposits a bank could accept under this facility).

- Another question to consider is whether green deposits must be a separate category. Whether setting aside a certain proportion of the individual bank’s outstanding deposits for green projects could serve as better option needs to be considered.

- The government may have to enter the picture and provide sops (like interest rate subvention or cover under PLI scheme) to make this possible. This would be helpful in attracting the smaller investors who are more focused on getting better returns.

Conclusion:

The green deposit regulation is progressive and comprehensive step. However, the scheme is expected to face many challenges as a result of the market forces’ role. Fine-tuning the framework according to market requirements would enable its success.

Practice Question for Mains:

What are the new regulations introduced by RBI for green deposits? What are the challenges and way ahead? (250 words)

If you like this post, please share your feedback in the comments section below so that we will upload more posts like this.